If someone asks you to jump into a pool, the first thing that you will ask is the depth of the pool. Now, assume that one person tells you that it is not too deep while the other tells you that it's 6 feet deep. Which response will you consider while making your decision to jump?

Most likely the latter, i.e., the pool is 6 feet deep. Similarly, when you are choosing an investment for your portfolio, which of the following responses would you prefer?

The investment will give good returns or the investment can potentially generate 6-8 percent returns. Again, as a rational individual, you will probably use the latter information. This brings us to the most important part of choosing an investment.

Calculating the returns.

Now, here is where most investors start losing sleep. What does Compounded Annual Growth Rate (CAGR) mean? Is it the same thing as simple interest? What is the concept of compounding?

Due to all this confusion, you are not only unable to calculate returns but might also find it difficult to compare returns of various instruments. We can simplify this for you by sharing just the right amount of information on return calculations.

The main aim of saving money and making investments is to preserve and grow the invested amount. For this purpose, it is important to accurately calculate the returns on your mutual fund investments.

Demystifying the different types of return calculations

Let's start this with an example. Pooja is a 28 year old working professional who has recently started her financial planning journey. Three years back, at the age of 25, she invested in a select mutual fund scheme. Below are the details of her investment.

Amount invested: Rs. 1,00,000

Net Asset Value (NAV)* of the scheme at the time of purchase: Rs. 10

Units bought: 10000 units

*The NAV of a scheme is the price at which the units of a scheme can be bought or redeemed. It is calculated as: NAV = (Total assets of the scheme – Total liabilities of the scheme) / Total number of units outstanding

Step by step guide to return calculations

Now, time to calculate returns

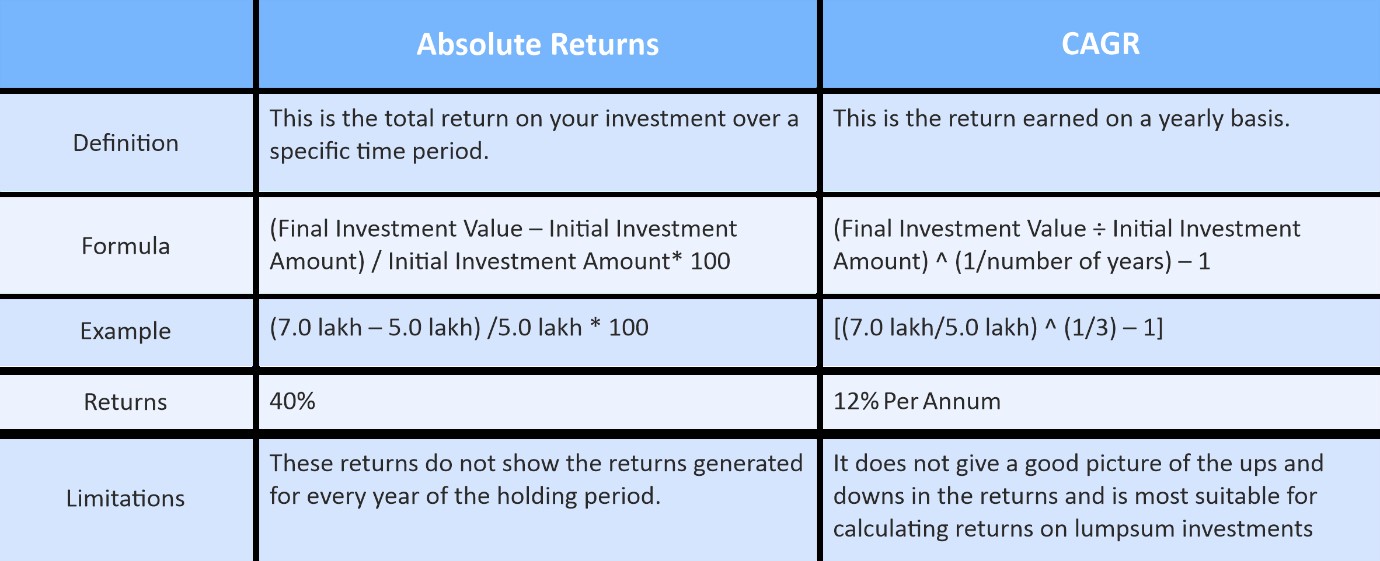

Absolute Returns

Absolute returns on a mutual fund investment reflect the change in value of the investment at the time of redemption or simply put, the gain or loss that you have made on the investment. It is the simplest form of calculating returns.

Assume that after three years, the NAV of the scheme in which Pooja invested is Rs. 15. This means that the total value of her investment today is:

Value of investment = NAV of the scheme x Total number of units held

= Rs. 15 x 10,000 units = Rs. 1,50,000

Now, let's calculate the absolute returns on Pooja's investment.

Absolute Return = (Final Investment Value – Initial Investment Amount) / Initial Investment Amount

* 100

Absolute return for Pooja = (1.50 lakh – 1.0 lakh) /1.0 lakh * 100 = 50%

Compounded Annual Growth Rate (CAGR)

This is the most common metric used to measure mutual fund returns. CAGR shows the average annual change in the value of an investment over a period of time.

Let's calculate the CAGR on Pooja's investment.

CAGR = (Final Investment Value ÷ Initial Investment Amount) ^ (1/number of years) – 1

Final investment value = Rs. 1.50 lakh

Initial investment value = Rs. 1 lakh

Number of years = 3

CAGR for Pooja = [(1.50 lakh/1 lakh) ^ (1/3) – 1] = approximately 14.5%

While CAGR gives a better picture of the performance of an investment when compared to absolute returns, it is important to note that it does not capture the variation in return. When you look at the above example, it would be natural to assume that the investment has grown at a rate of 14.5% every year. However, that might not always be the case. In some years it could have gone up by 35% while in others it could have gone down by 5%. However, CAGR will not show you the up and down movements in returns.

Another thing to note about CAGR is that it is best used in the case of lumpsum investments that are point-to-point in nature. It cannot capture periodic investments made via the Systematic Investment Plan (SIP) route.

Difference between Absolute Returns and CAGR

Extended Internal Rate of Return (XIRR)

As highlighted above, CAGR is a good metric to measure returns from lumpsum investments but not suitable for investments where there are multiple cashflows like SIPs. An SIP is basically an investment vehicle that allows you to invest a fixed amount of money into a mutual fund scheme of your choice at time intervals that suit you best. So, you could choose to start a fortnightly SIP, a monthly SIP or even a quarterly SIP.

Thus, every SIP instalment is an investment for a different period of time. For example, when you start a 3-year monthly SIP, the first instalment is invested for 36 months, the second instalment is invested for 35 months, the third instalment is 34 months, and so on. The NAV at which each instalment is done will most likely differ and so will the returns on each instalment

XIRR is calculated by arriving at the CAGR for each instalment and then adding it together to arrive at the overall CAGR. The steps in calculating XIRR include:

- Calculate CAGR for the first instalment assuming the investment period to be 36 months.

- Calculate the CAGR for the second instalment assuming the investment period to be 35 months.

- Keep reducing the time period till you reach the last instalment – calculate the CAGR for the last instalment assuming the investment time period to be 1 month.

You must note that the NAV at which you buy each instalment will differ as each instalment is invested at a different time. Once you have calculated the CAGR for each instalment, add it up to arrive at the XIRR.

This way, XIRR can be an ideal method to calculate returns on investments made via the SIP route as they can easily capture the returns made on each SIP instalment.

Many of the above calculations can easily be done using a mutual fund return calculator. You simply need to input the principal amount, the investment time period, and the expected rate of return to calculate the final maturity amount. Conversely, you can also input the initial investment amount, the investment time period, and the expected maturity value to determine the expected rate of return on the investment. Once you know the rate of return, making the investment decision will become much easier.

With this, knowing and calculating investment returns will become easy. Now, you can use the right return calculation to estimate the returns on your mutual fund investments and make more informed investment decisions.

An investor education initiative by Edelweiss Mutual Fund

All Mutual Fund Investors have to go through a onetime KYC process. Investor should deal only with Registered Mutual Fund (RMF). For more info on KYC, RMF and procedure to lodge/redress any complaints, visit -https://www.edelweissmf.com/kyc-norms

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS,READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

Solution For you

Solution For you  Equity Funds

Equity Funds Hybrid Funds

Hybrid Funds Debt Funds

Debt Funds Equity Index Funds/ETFs

Equity Index Funds/ETFs Precious Metals

Precious Metals SIP/STP & More

SIP/STP & More SIP Calculator

SIP Calculator Retirement Planning Calculator

Retirement Planning Calculator STP Calculator

STP Calculator SWP calculator /

SWP calculator / SIP performance calculator

SIP performance calculator Mutual Fund Return calculator

Mutual Fund Return calculator Lumpsum calculator

Lumpsum calculator Webinars

Webinars Investment Insights

Investment Insights Book Summaries

Book Summaries Edelweiss Klassroom

Edelweiss Klassroom Account Statement

Account Statement Modify SIP

Modify SIP Update Profile

Update Profile Transaction Status

Transaction Status Update KYC Status

Update KYC Status Transaction Status

Transaction Status Create personalized link

Create personalized link